SOFTWARE DESIGNED WITH YOUR Growth

IN MIND

Scale your evolving business and grow

revenue efficiently with a range of

comprehensive software solutions from Rev.io

.webp?width=684&height=273&name=LogoOnly_MARCO_FullColor-DRK%20(1).webp)

REVENUE LEAKAGE

You shouldn’t have to worry about quoting, billing, and collecting payments at scale. We help you identify and capture lost revenue across your entire company.

-3.svg)

GROWING PAINS

Common growth blockers include telecom usage rating issues, tax problems, and systems that don’t scale. With Rev.io, these challenges are easier to overcome.

POOR CUSTOMER EXPERIENCE

Existing processes and systems may be creating CX issues and churn risks. Rev.io can help improve your customer retention and overall customer experience.

-2.svg)

-1.svg)

OUT OF CONTROL COSTS

Are you losing time and money to swivel chairing, frequent manual errors, and inefficiencies caused by using multiple systems? Rev.io’s solutions can help.

LACK OF VISIBILITY

You can't see all your essential data, people, projects, inventory, or bills in one system and it's slowing you down. With Rev.io, all the information you need is in one place.

-Jan-13-2024-06-57-47-6218-AM.svg)

-Jan-13-2024-07-42-59-7587-AM.svg)

INADEQUATE SUPPORT

You shouldn’t be expected to rely on support you can’t depend on. The Rev.io team takes enormous pride in the support behind the software that we provide to our customers.

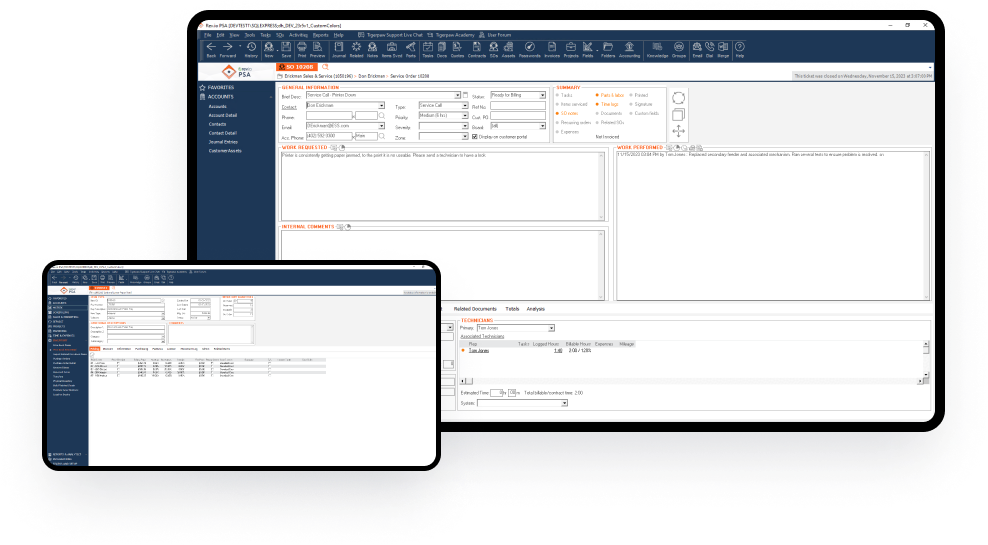

Rev.io Billing is an automated platform that covers every unique aspect of the complex quote-to-cash process.

Automate time-consuming processes so your entire team can focus on their top priorities: growth, efficiency, and customer experience.

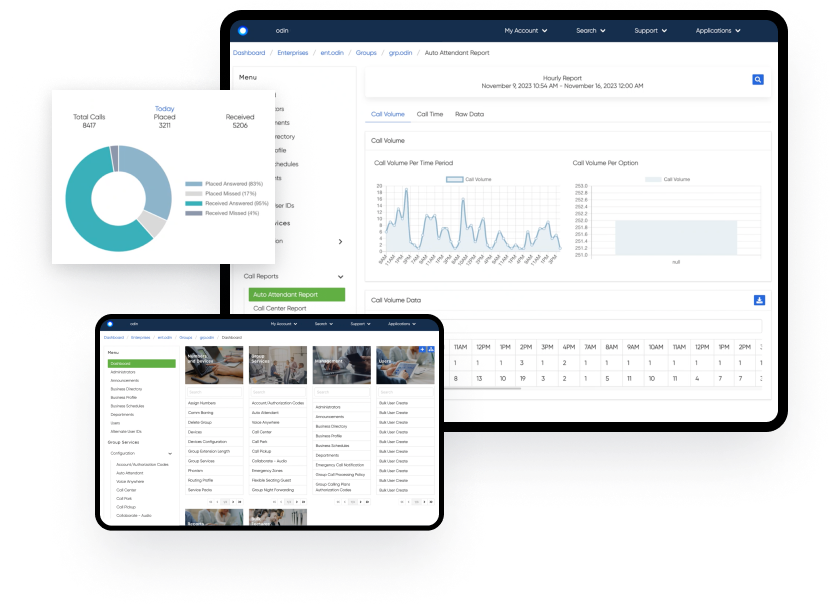

Rev.io Odin enables communication service providers using Cisco Broadworks to evolve with new features, functionality, and integrations.

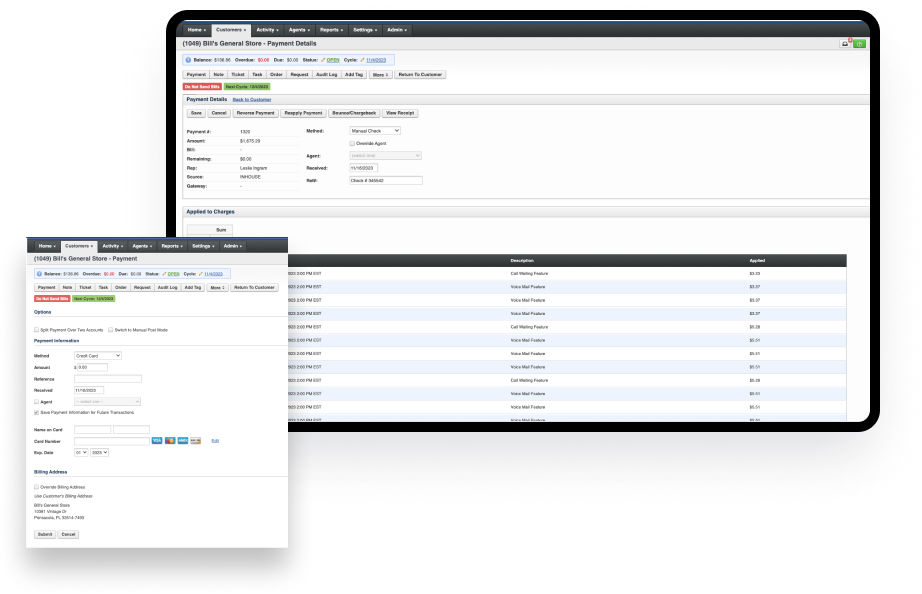

Optimize the final stage of your quote-to-cash experience with Rev.io Payments, our fully integrated merchant processing platform.

With Rev.io Analytics, our dynamic billing analytics and KPI solution, you can use your most critical data to help you manage a smarter business.

Rev.io's solution has effectively resolved the challenges faced by GigTel in tracking agent activity and managing commissions as well as billing and tax complications. This improvement streamlines operations, enhances productivity, and positions GigTel for future expansion in their agent channel.

Thomas Forajter | VP of Operations

Rev.io has really been a huge part in our success...because we have to bill our customers for a ton of different services that we provide to them. Because of Rev.io being so flexible, we have been able to grow a huge amount with Rev.io.

Christian Hernandez | Founder and CEO

We needed a reliable and capable billing partner that simplified our backend processes...Rev.io brought all of our reporting and different billing processes all into one program.

Alexander Rodgers | Operations Manager

Since our move to Rev.io, it is scary how much more revenue we are accounting for compared to our previous system. We have been able to minimize the manual processes necessary to get invoices out, which has lowered our labor costs.

Tom Welsh | President

-Jan-18-2024-09-22-42-1290-AM.svg)

01. DEMO

After an initial discovery call, we’ll show you how Rev.io’s solutions can solve your company’s current frustrations.

-Jan-18-2024-09-14-36-6498-AM.svg)

02. CONFIGURE

Next, our experts will configure a solution specific to your business needs for your approval.

03. ONBOARD

Once approved, we’ll begin onboarding and training, so your team will be ready to go when it’s time to activate.

-Jan-18-2024-09-16-48-0275-AM.svg)

-Jan-18-2024-09-19-28-6886-AM.svg)

04. ACTIVATE

Finally, we’ll activate Rev.io software and the Rev.io team will act as partners in your business’ continued success.

%201.svg)

CLIENT SUCCESS STORIES

See how some of our most successful clients are winning with the help of Rev.io.

PRIMEVOX COMMUNICATIONS

Mental models are simple expressions of complex processes or relationships.

AFFILIATED TECHNOLOGY SOLUTIONS

Realized a 5:1 ROI after activating on Rev.io.

GIGTEL

GigTel relies on Rev.io to support a UCaaS Launch

JCM TELECOM

Doubled their revenue with the help of Rev.io.